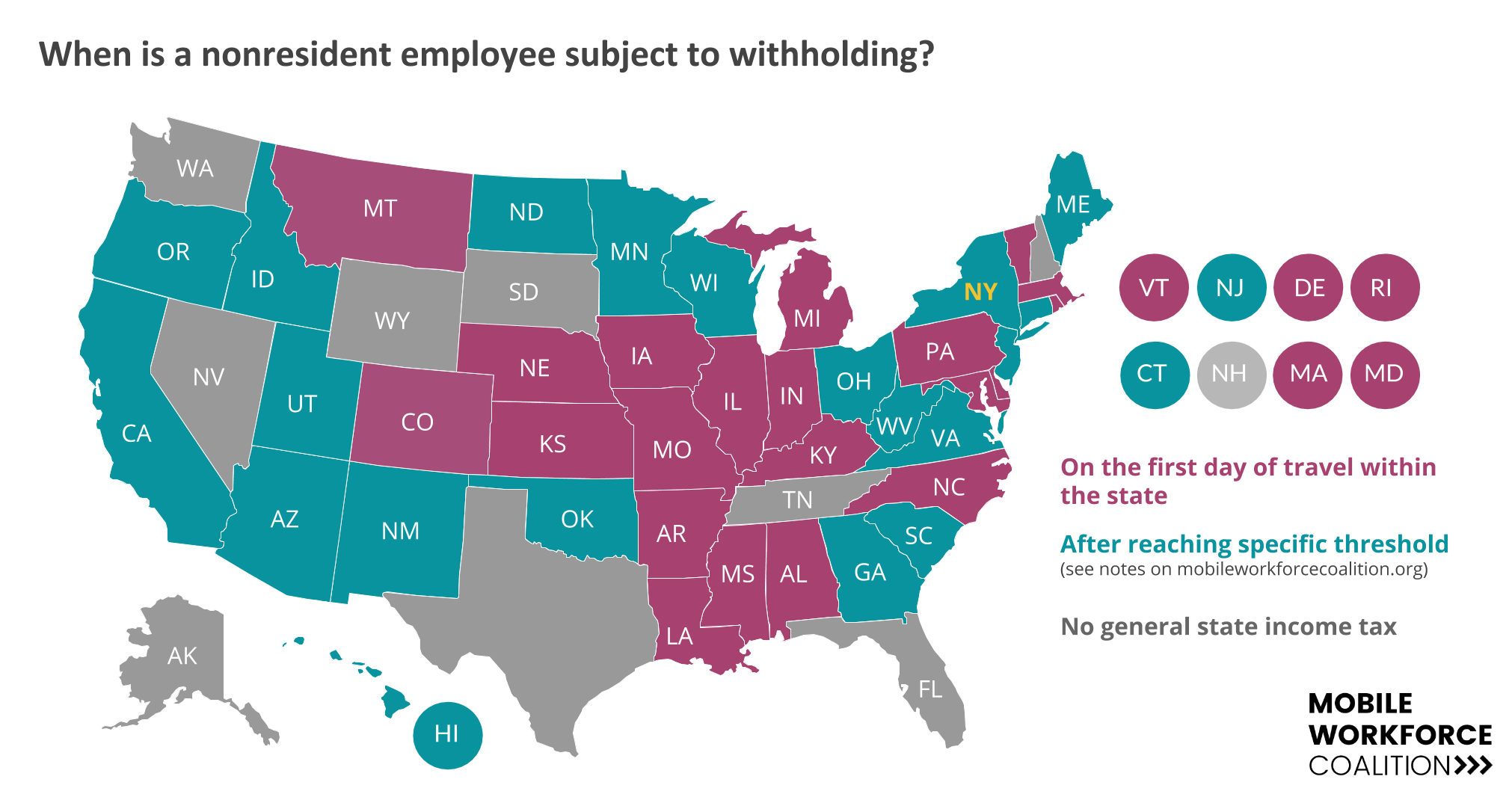

Do you travel across state lines for work? You might owe nonresident state income tax if you do. Most states technically require tax payments when you’re in the state for even a day (see map below), and that withholding should be set up in advance. It’s been a headache for business travelers and companies for years. Now, legislation pending in the Senate may change the game.

On June 20, 2017, the U.S. House of Representatives passed HB 1393, the Mobile Workforce State Income Tax Simplification Act of 2017, via voice vote. The bipartisan bill is designed simplify state income tax rules for employees who travel across state lines, and prohibit state taxation of wages or other remuneration earned by an employee who performs employment in more than one state other than by:

In other words, the bill prevents a state from collecting nonresident state income tax on employees who work in the state for 30 days or less in a calendar year.

Instead, HB 1393 would create a uniform national standard, eliminating the compliance nightmares faced by many employers and traveling employees who need to keep track of numerous state income tax withholding laws and varying de minimis exemption periods. The bill covers all employees, as defined under state law, with the exception of professional athletes and entertainers, qualified production employees, and certain public figures. After 30 days, existing state laws would apply.

Proponents of the bill claim existing tax laws disrupt interstate commerce and falsely suggest that business travelers earn their income in traveling states and not the home office. Organizations like the AICPA stand in solidarity, claiming that bill would eliminate the need for much of the complex recordkeeping that employers and employees face when crossing state lines to work. The introduction of a uniform 30-day rule would bring welcome certainty to the taxation of business travelers and mobile employees, facilitating tax and employment planning. Employers, supporters claim, would save a considerable amount money in compliance and administrative costs.

A uniform national standard is generally opposed by large states that stand to lose millions in revenue, most notably New York, which sees an abnormally large number of business travelers each year (NY stands to lose anywhere between $55M and $120M in revenue, according to CBO estimates). All states with a large employment centers close to a state border (hello, Charlotte) stand to lose more.

An identical bill has been introduced in the Senate, and although a review date is not certain, it enjoys bipartisan support. If enacted, the legislation will take effect on January 1 of the second calendar year that begins after the date of the enactment.

It seems like there’s an overall movement in Congress for tax simplification. This measure is one of several bills on the table that are designed to update states’ taxing power in an increasingly interconnected economy. We’re watching all of them. Stay tuned.

{kind=link}