Published on February 29, 2012. Article written by .

In an earlier post regarding the Laffer Curve, I explained the concept that there is a relationship between rates and government revenues - and that it is a curve effect (e.g. if the rate is 100%, the government would receive no revenue as there would be no economy – however at zero the government does not receive revenue either).

Recently I came across a paper by Nicholas Paleveda of Northeastern University that attempts to explain the correlation between tax rates and economic growth. In his paper, Mr. Paleveda evaluated, since the 1950s, the corresponding highest marginal tax rates and the corresponding economic growth rate as measured by growth in the S&P 500. His question was 'do income tax rates kill corporate growth' as measured by growth in the S&P 500.

Interestingly, what Mr. Paleveda found is that lower marginal rates historically have hurt the S&P while higher rates have corresponded to higher growth in the S&P. He also postulates that the optimal highest marginal individual income tax rate should be around 39% - 50% - which, incidentally, is definitely higher than the current Republican presidential contenders have proposed but also higher, by a small amount, than the expiration of the Bush era tax cuts that are set to expire in 2013.

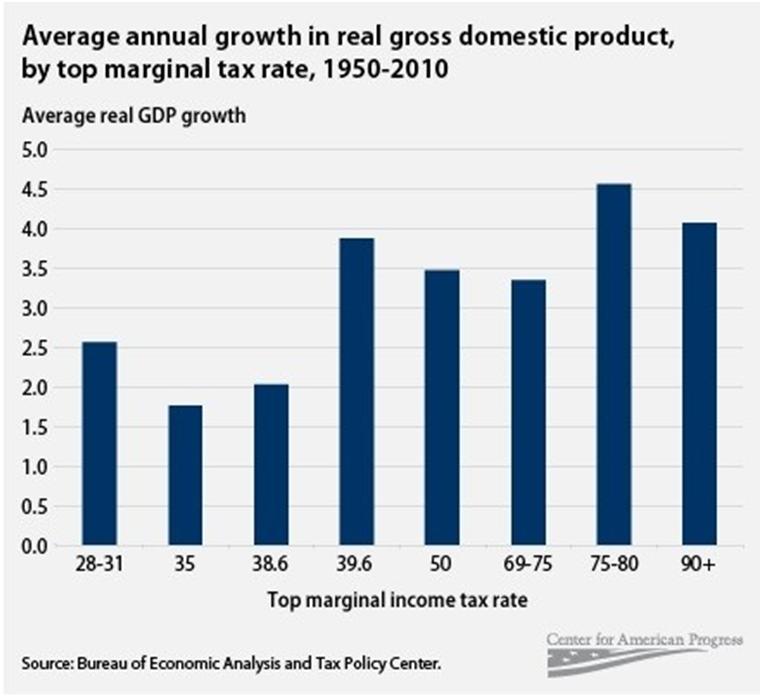

Interestingly this theory was also tested by the Bureau of Economic Analysis and Tax Policy Center and is the subject of a blog by the Washington Post. When measured against GPD growth, there has not been a correlation between low rates and growth – the contrary has been true.

While neither author definitely states that we should raise tax rates, both suggest that if lower marginal rates correspond to periods of excessive deficits that require borrowing and reduced government services (as they do now) perhaps those actions in themselves weaken confidence which subsequently drives down the S&P.

Currently, the S&P has done well over the last few years – only because it rebounded from a significant trough. There has not been any real growth in the S&P since 2007; most of the returns today are related to higher profits due to cost cutting measures, not real growth in sales – so our rates at this level when graphed would indicate no real growth in the S&P or the GDP.

This analysis would seem to imply that either spending needs to go down and / or rates need to go up in order to drive growth, but simply lowering rates in itself does not appear to have a historical correlation to real economic growth.

What do you think?

About the author:

Adam Boatsman is the Owner / Visionary at BGW Advisors.

CPA License: NC #34370

Learn more about Adam and the rest of our team on the Team page.